July 20, 2026

AI Demand Fuels High-End MLCC Demand, Japanese and Korean Manufacturers See Record High Book-to-Book (BB) Ratios, Supply Shortage Risk Rises in Second Half of the Year

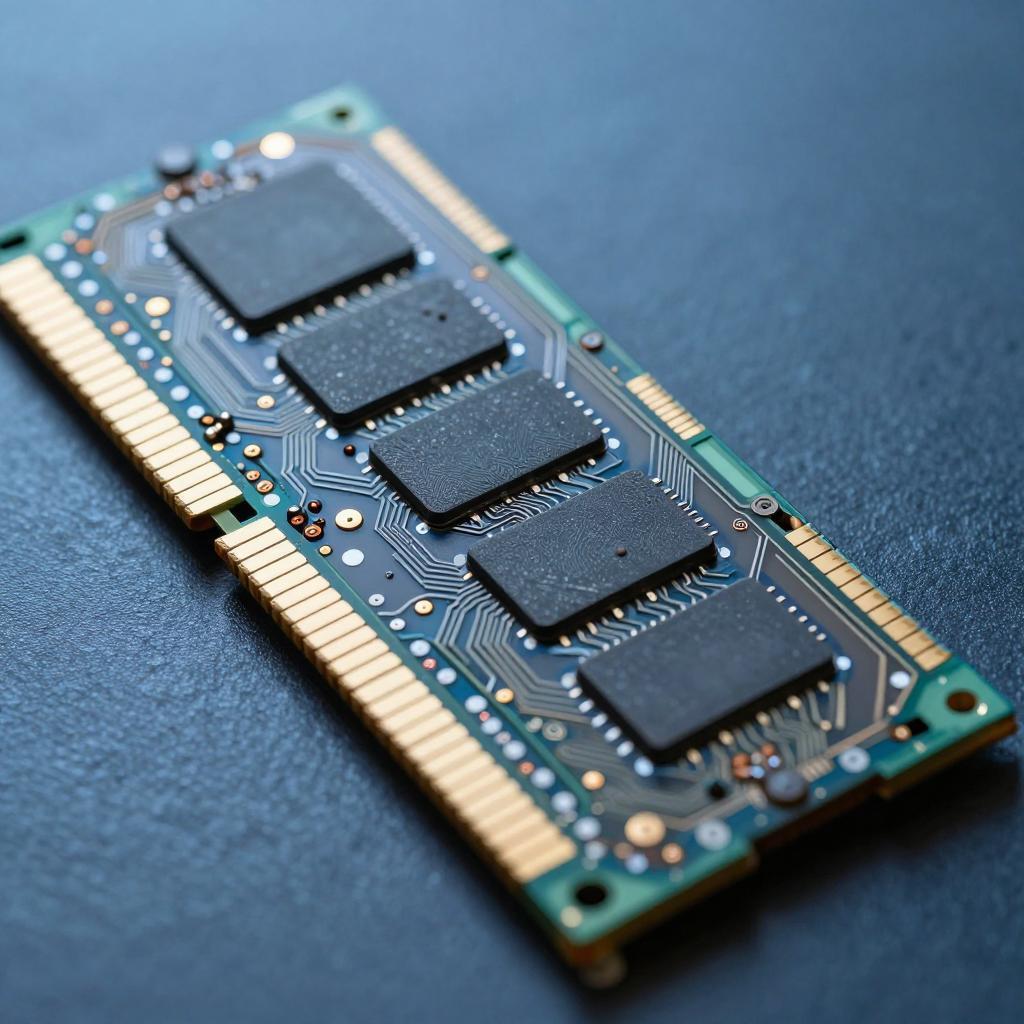

AI Demand Fuels High-End MLCC Demand, Japanese and Korean Manufacturers See Record High Book-to-Book (BB) Ratios, Supply Shortage Risk Rises in Second Half of the Year July 17, 2026 — A recent TrendForce report shows that upgrades to AI server platforms and the continued ramp-up of CSP's self-developed ASICs are rapidly driving demand for high-end MLCCs. As of late June, the BB ratios of Murata, Samsung Electro-Mechanics, and Taiyo Yuden, the three leading Japanese and Korean manufacturers, rose to 1.30, 1.31, and 1.25 respectively, reaching new highs since the pandemic, while the overall industry BB ratio climbed to 1.04. Murata's Q1 financial report is particularly noteworthy: its order backlog ratio reached 1.27, exceeding the peak of 1.25 at the beginning of the most severe MLCC shortage in 2018, indicating that backlogged orders are accumulating rapidly and the risk of supply shortages is intensifying. Demand shows a significant divergence between hot and cold markets. According to TrendForce, the US CPI rose 4.2% year-on-year in May, with high interest rates continuing to suppress consumer purchasing power, putting pressure on demand for smartphones and laptops. Intel and AMD are also prioritizing CPU production capacity for AI applications, squeezing traditional PC supply and forcing ODMs to shift to rush orders, further driving up material costs. In stark contrast, mass production of AI custom accelerator platforms such as Google TPU, AWS Trainium, and Meta MTIA is ramping up, continuously driving up demand for high-capacitance, low-voltage, and miniaturized MLCCs. The supply-side squeeze has spread to the automotive and consumer electronics sectors. Apple's supply chain started stockpiling one to two months earlier than usual, and automotive ODMs have also shifted their procurement schedule from July to May, reflecting widespread market concerns about a supply gap in the second half of the year. In the Chinese market, distributors have raised prices for mainstream consumer-grade X5R MLCCs since June, with an average increase of 15%–25%, further exacerbating market tensions. Taiwanese and mainland Chinese manufacturers are seeing a surge in orders from overseas markets. With Japanese and Korean manufacturers continuing to prioritize orders for high-end AI MLCCs, TrendForce predicts that Yageo, Walsin Technology, and Microcapacitor will benefit from the spillover demand for mid-to-high capacitance consumer-grade X5R MLCCs in Q3. Looking ahead to the second half of the year, Q4 may be a key turning point. Starting in Q3, NVIDIA, Google, and AMD's next-generation AI platforms will enter mass production, and capacity utilization is expected to remain highly concentrated on AI orders. Coupled with customers stockpiling inventory, lead times for high-end MLCCs are expected to extend, and prices may rise further. TrendForce believes that Q4 will be a crucial period for determining whether the high-end ML...

View More

![Celebrating Two Decades of Deep Cultivation and Embracing the Dragon Boat Festival: A Letter from [GHT] to All Partners and Customers](/uploadfile/news/f92997147f723ef9bb430fd68f72812d.jpeg)

![Celebrating Two Decades of Deep Cultivation and Embracing the Dragon Boat Festival: A Letter from [GHT] to All Partners and Customers](/uploadfile/news/90016511d1a2289dd83a92100a835bd7.jpeg)